Indian equities kicked off the week on a strong note, with bulls charging through Dalal Street as an Iran-US peace framework and sliding oil prices lifted the Sensex and Nifty over 1.5% each, mirroring gains across global markets.

The sharp gains added nearly Rs 8 lakh crore to the total market capitalisation of all companies listed on BSE, pulling it up to around Rs 470 lakh crore.

IndiGo, Bajaj Finance, Eternal, UltraTech Cement, L&T, Bajaj Finserv, Maruti Suzuki, Asian Paints, Trent, HDFC Bank, M&M, Infosys, Titan, Infosys, Adani Ports, Hindustan Unilever, Tata Steel, SBI and Tech Mahindra shares jumped 1-4% to lead gains on Sensex, while Sun Pharma and Bharti Airtel slipped into the red with marginal losses.

Broader markets also gained sharply, with Nifty Midcap 100 and Nifty Smallcap 100 indices gaining up to 1.5%. This came as India VIX, which measures volatility in markets, dropped 4% to 14.13. Sectorally, Nifty Realty and Nifty Financial Services surged around 3% to lead gains. Nifty Pharma however slipped into the red. The overall market breadth was strongly positive, with 2,491 stocks advancing on NSE, while 241 declined and 74 remained unchanged.

Here are the key factors pushing the stock market higher today:

1) Iran-US reach peace deal framework

US President Donald Trump announced on Sunday that the much-awaited agreement has been finalised. "The Deal with the Islamic Republic of Iran is now complete," Trump wrote on his Truth Social platform. He further said that the Strait of Hormuz, a vital route for global oil shipments that Iran has effectively closed for months, would reopen on Friday, while the US would end its blockade of Iranian ports. "Ships of the World, start your engines. Let the oil flow!" Trump wrote.

Iran meanwhile said that the newly announced agreement with the United States puts an "immediate end" to the countries' war. "A permanent and immediate end to the war has been declared on all fronts, including Lebanon," Iran's Deputy Foreign Minister Kazem Gharibabadi said in televised comments in the early hours of Monday.

The peace deal framework brought much needed relief to oil prices, which had soared to as high as $120 per barrel earlier this year following closure of the Strait of Hormuz, a narrow 33-kilometre waterway connecting the Persian Gulf with the Gulf of Oman that handles over 20% of the world’s daily oil and gas shipments.

Brent crude futures declined around 5% to trade near $83 per barrel, while WTI Crude futures tumbled 6% to $80 per barrel on Monday morning.

Amid the risk-off sentiment, US Treasury yields dropped. The yield on benchmark US 10-year notes fell sharply to 4.426% while the 30-year bond yield dropped to 4.924. The 2-year note yield, which typically moves in step with interest rate expectations for the Federal Reserve, fell to 4.024%. Falling bond yields typically make bonds less attractive to investors, which in turn can lead to some uptrend in markets.

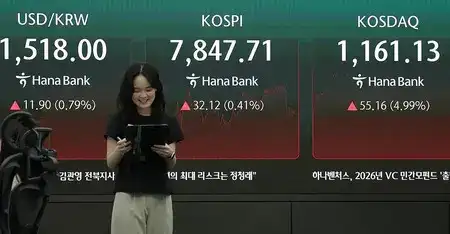

As a result of the renewed optimism, global markets rallied, with Dalal Street being no exception. Japan’s Nikkei jumped more than 5% while South Korea’s Kospi rallied around 6%. Hong Kong’s Hang Seng and China’s Shanghai Composite were up nearly 1% each, while Taiwan Weighted rallied around 3%.

Wall Street had ended the last session with minor gains, with the tech-heavy Nasdaq gaining 0.3% on Friday. European markets made strong gains on Friday, with UK’s FTSE, France’s CAC and Germany’s DAX jumping around 2% each.

5) Rupee strengthens past 94

Rupee gained 53 paise to 93.65 against the US dollar in early trade. The weekend news flow will be crucial, Jateen Trivedi, VP Research Analyst - Commodity and Currency at LKP Securities had highlighted. “If there are no adverse developments regarding geopolitical negotiations, the rupee could attempt to break the important 94.80 resistance zone, which remains a key technical level on a closing basis. For the near term, rupee is expected to trade between 94.80–95.50. A sustained move below 94.80 could trigger a stronger recovery towards the 94.00 level in the coming sessions,” he said. Notably, the Indian currently has now breached the key technical levels suggested by the analyst.

What lies ahead for Indian stock market?

"With the dawn of peace in West Asia, hopefully, and the consequent sharp correction in Brent crude to below $84 in early trade, the prospects for the Indian economy and stock market have turned for the better, said VK Vijayakumar, Chief Investment Strategist at Geojit Investments.

He added that the GDP growth rate and CPI inflation projections for FY27 can be revised in this changed scenario to 6.9% and 4.6% respectively. This will have positive implications for the stock market, according to the analyst.

While Vijayakumar expects the rupee to continue its uptrend and dip below 95 to the dollar, he highlights that FPIs are unlikely to continue big selling in India even though the AI trade still continues to be strong, particularly in South Korea and Taiwan. “Domestic money - retail plus DIIs- will drive the market higher today on the back of the smart gains last Friday,” he said.

“Banks are likely to lead the rally. The big short positions in the leading private sector banks will continue to trigger further short covering in the segment. Their valuations are attractive in this fairly valued market. Nifty Mid cap at 29 times and Nifty Small cap at 33 times earnings are overvalued compared to the Nifty which is trading at around 20 times.However, the better performance of the broader market in Q4 FY26 and better earnings prospects in FY 27 will continue to attract investment into this segment,” he concluded.

From the vicinity of lower bollinger band, just the other day, Nifty now aims for the upper bollinger band, which is now at 24,029, according to Anand James, Chief Market Strategist at Geojit Investments. He however expects the market to see volatility, once Nifty is in the vicinity of 23,900. While a close near 23,700 could point to consolidation, a direct rise above 24,029, will spark the next leg of upsides aiming 24,300-24,600, he said, adding that this though is less expected right away.

Going ahead, we expect the index to maintain positive bias and head towards 23,800 and 24,050 levels in the coming sessions being the confluence of the 50 days EMA and higher band of the last 2 months falling channel and the measuring implication of the recent range breakout (23,050 - 23,550). Volatility is likely to remain high on account of the volatile global cues. We believe index holding above the 23,500 - 23,300 levels will keep the bias positive being the confluence of last week's breakout area and Friday’s low,” said Bajaj Broking.